The Problem

In 2018, the biggest threat to traditional banks wasn’t fintech startups. It was Apple, Amazon, Google, and Alibaba. These companies had spent a decade building something banks hadn’t: algorithmic understanding of human behaviour at scale. They could sift massive datasets and derive consumer insights in seconds. And they were entering financial services not as outsiders, but as companies that already owned the customer relationship.

A leading bank in Southeast Asia — one of the largest in the region — was staring at this reality. They had the regulatory moat, the capital reserves, the trust. What they didn’t have was a product strategy for a world where invisible banking was the competitive frontier. Not invisible as in “hard to find,” but invisible as in “so seamlessly woven into daily life that you stop noticing it’s there.”

The question wasn’t whether digital banking mattered. Every bank had an app by then. The real question was harder: how does a traditional institution, built around branches and relationship managers, redesign itself around algorithms and ambient financial services? Where do you even start when the competitive advantage shifts from physical presence to data fluency? That’s what I was brought in to figure out.

The Approach

I started where most product work should start and rarely does — understanding the institution’s actual strategic position, not just its stated ambitions. I analysed the bank’s recent leadership announcements, ongoing innovation initiatives, and competitive landscape. This included mapping emerging digital-only banks alongside traditional competitors to identify where the real differentiation gaps existed. The goal wasn’t a feature comparison — it was understanding which strategic moves were available and which were foreclosed.

Next, I went deep on customer pain points, specifically targeting the millennial segment that represented the bank’s growth demographic. I reviewed consumer behaviour reports and case studies to identify expectations, friction points, and underserved needs. What emerged was a pattern: younger customers didn’t want “better banking.” They wanted banking that didn’t feel like banking at all. They wanted their financial life to work the way their messaging apps and ride-hailing services did — anticipatory, conversational, ambient.

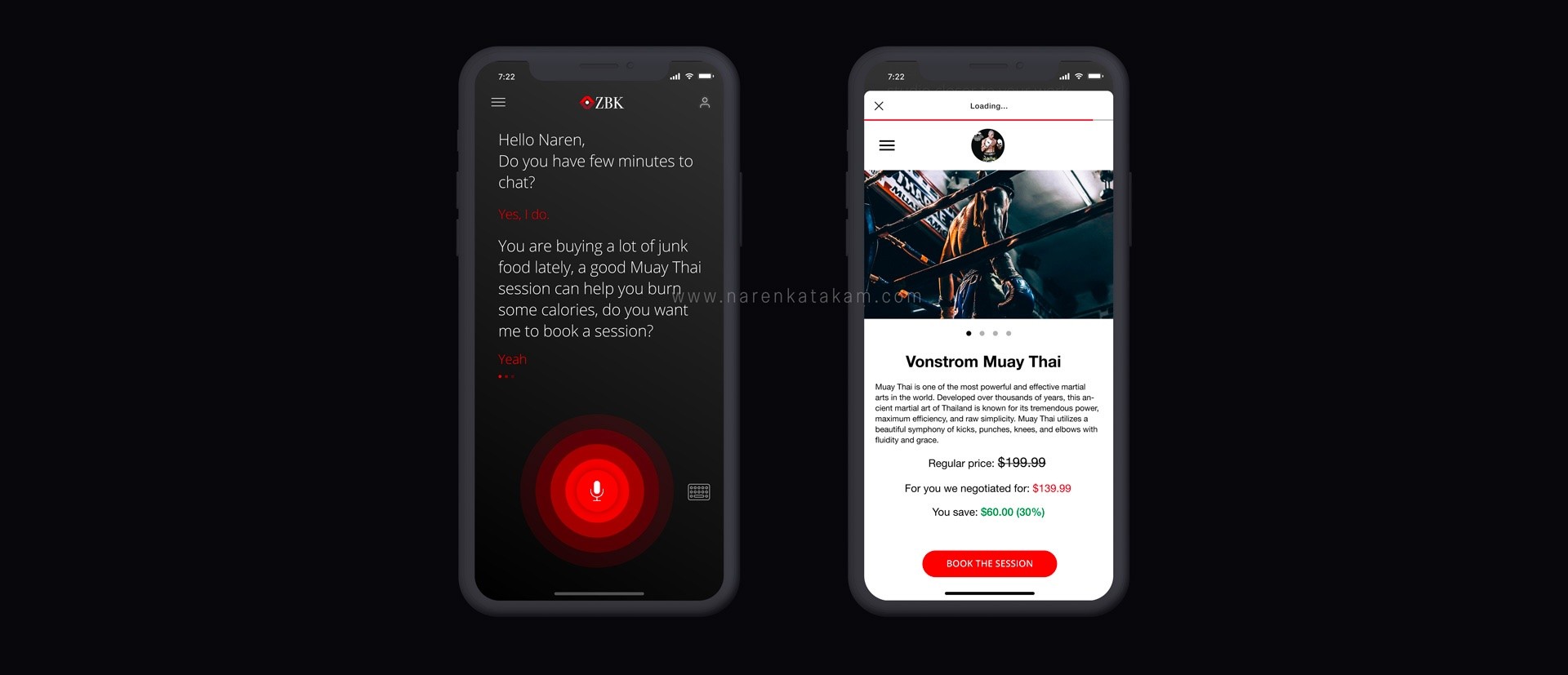

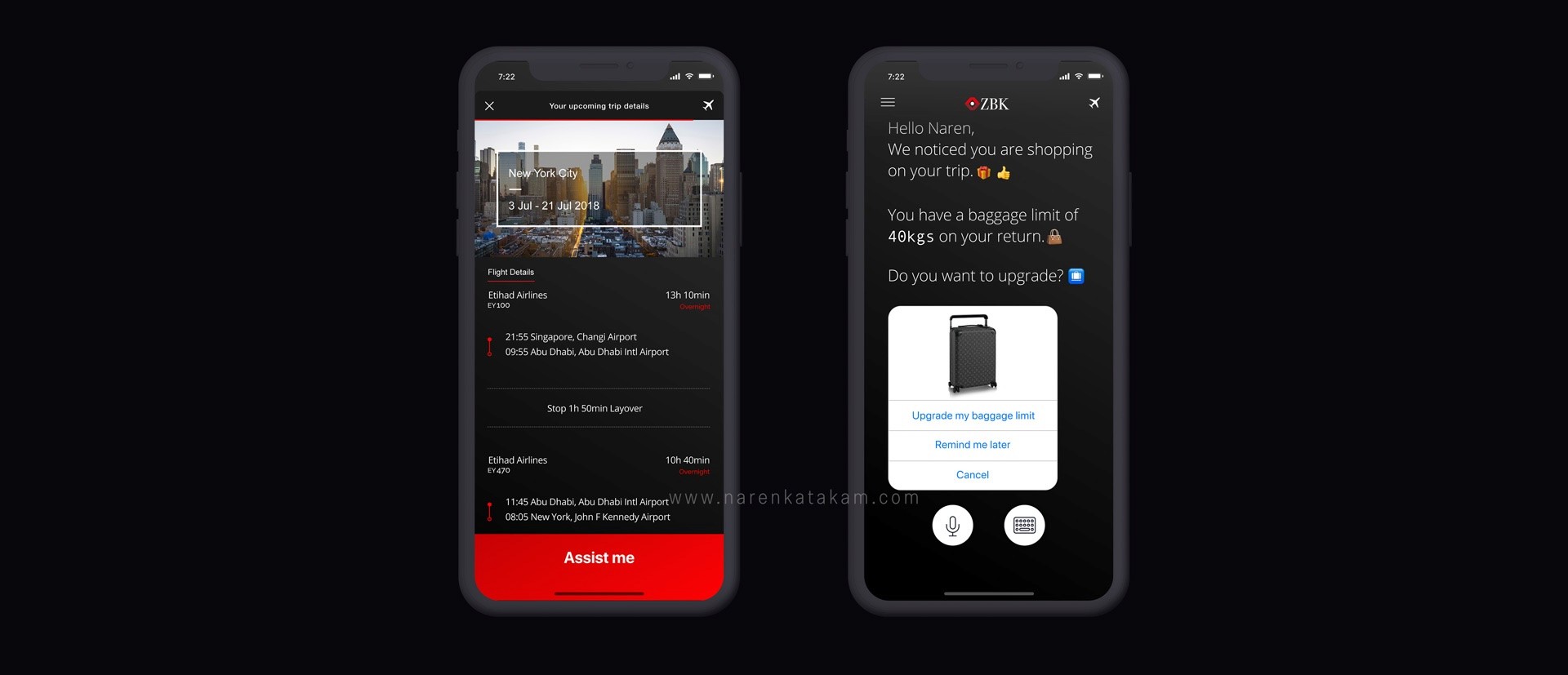

The behavioural data insight was formative — I mapped solutions directly to those pain points. Not a feature wishlist, but a deliberate mapping of each friction point to a specific capability that would resolve it. I set out a bold vision for the product design: can a user do banking while they do their workout? For me, this was a proof of concept — a thin slice of the invisible banking experience. I designed a new customer journey showing how conversational banking could be embedded into daily activities rather than existing as a separate destination.

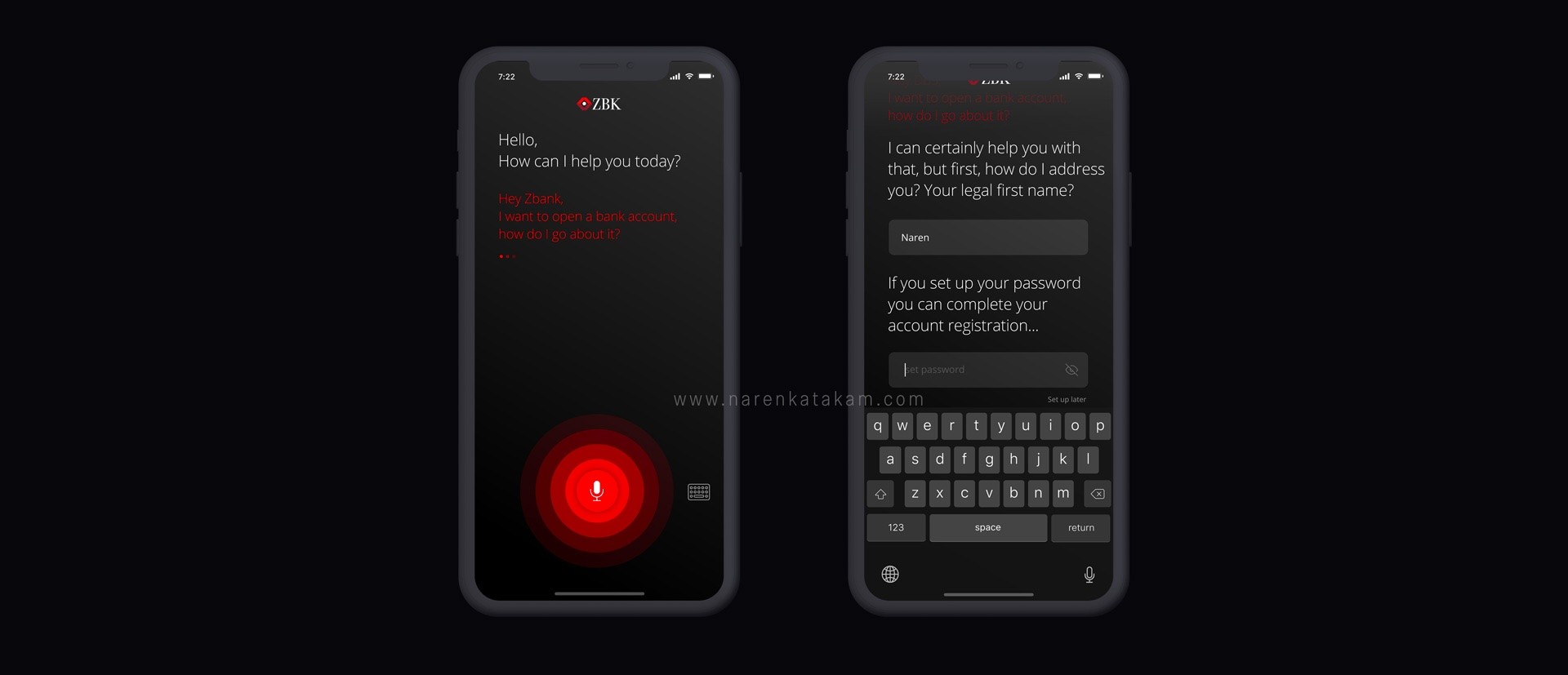

The final stage was technical validation. I worked with engineering teams to assess feasibility against the bank’s existing backend systems. We identified emerging technologies — biometrics, location services, computer vision, natural language processing — that could support the envisioned journeys. After evaluating options, we zeroed in on the RASA stack for the conversational layer. RASA’s intent and entity extraction capabilities impressed me — but more than that, it gave me a way to understand conversations philosophically. Dissecting a sentence to separate intent from entities taught me the nuance of dialogue at its most structural level. This was the pre-”token-in, token-out” era, where understanding the backbone of conversations mattered more than the end product. LLMs have since abstracted that work away, but the foundational understanding of conversational design still shapes how I think about human-AI interaction. After validation, I built interactive prototypes that brought the new journeys to life.

What We Deliberately Didn’t Build

The core design insight was subtraction: removing the seams between banking and daily life, not adding more banking features.

- Didn’t build a “better banking app.” We rejected the entire app-as-destination paradigm. The goal was to make the bank disappear into daily routines, not to win an app store design award.

- Didn’t add features to the existing mobile banking experience. We designed a fundamentally different interaction model — ambient and conversational — rather than iterating on the old one.

- Didn’t build a chatbot that answers banking questions. We built a proactive assistant that initiates conversations based on behavioural signals. The difference matters: a chatbot waits for you to have a problem. A behavioural banking assistant anticipates the problem before you articulate it.

- Didn’t start from the bank’s product catalog. We started from the customer’s daily routine and worked backwards to the financial services that should be embedded within it.

Every feature we cut made the product sharper. The discipline of via negativa — Taleb’s principle that what you remove defines a system more than what you add — became a core design philosophy I’ve carried into every project since.

What We Built

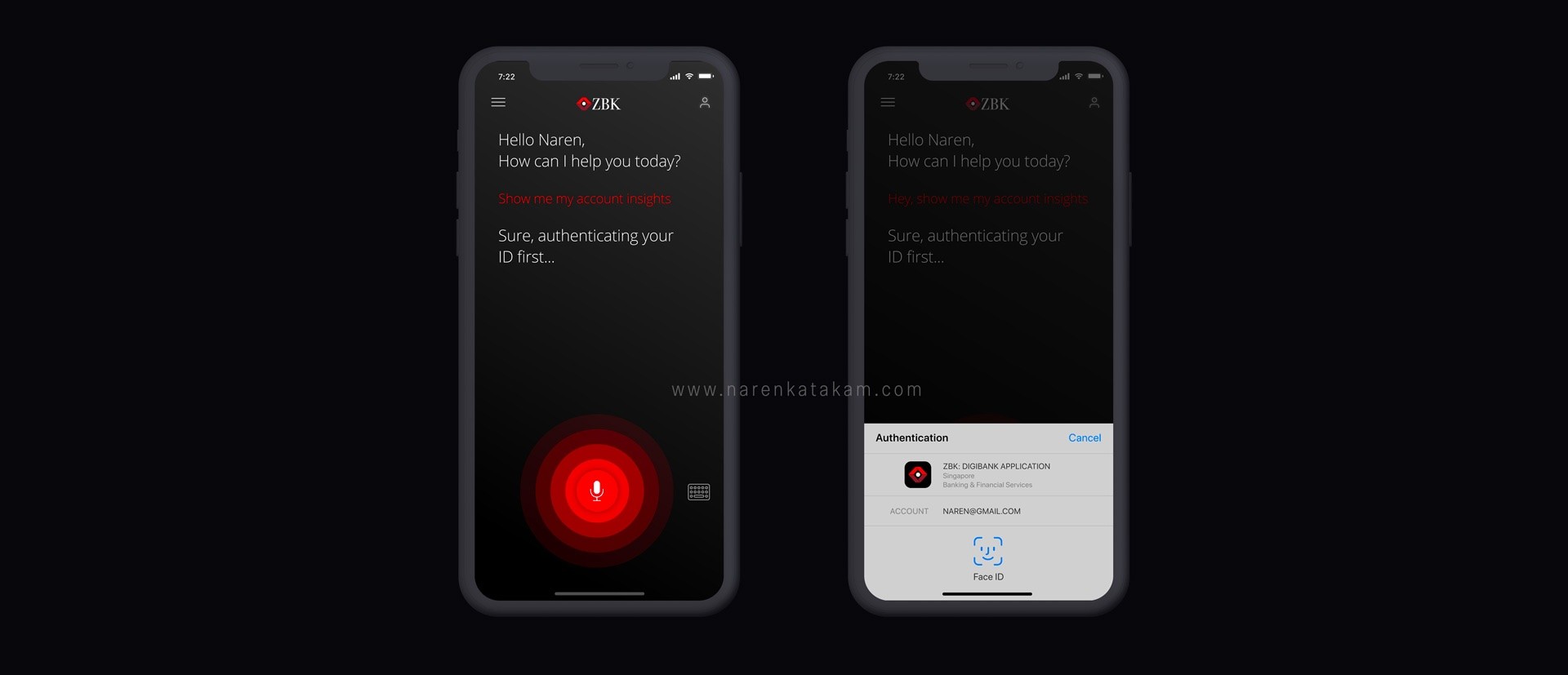

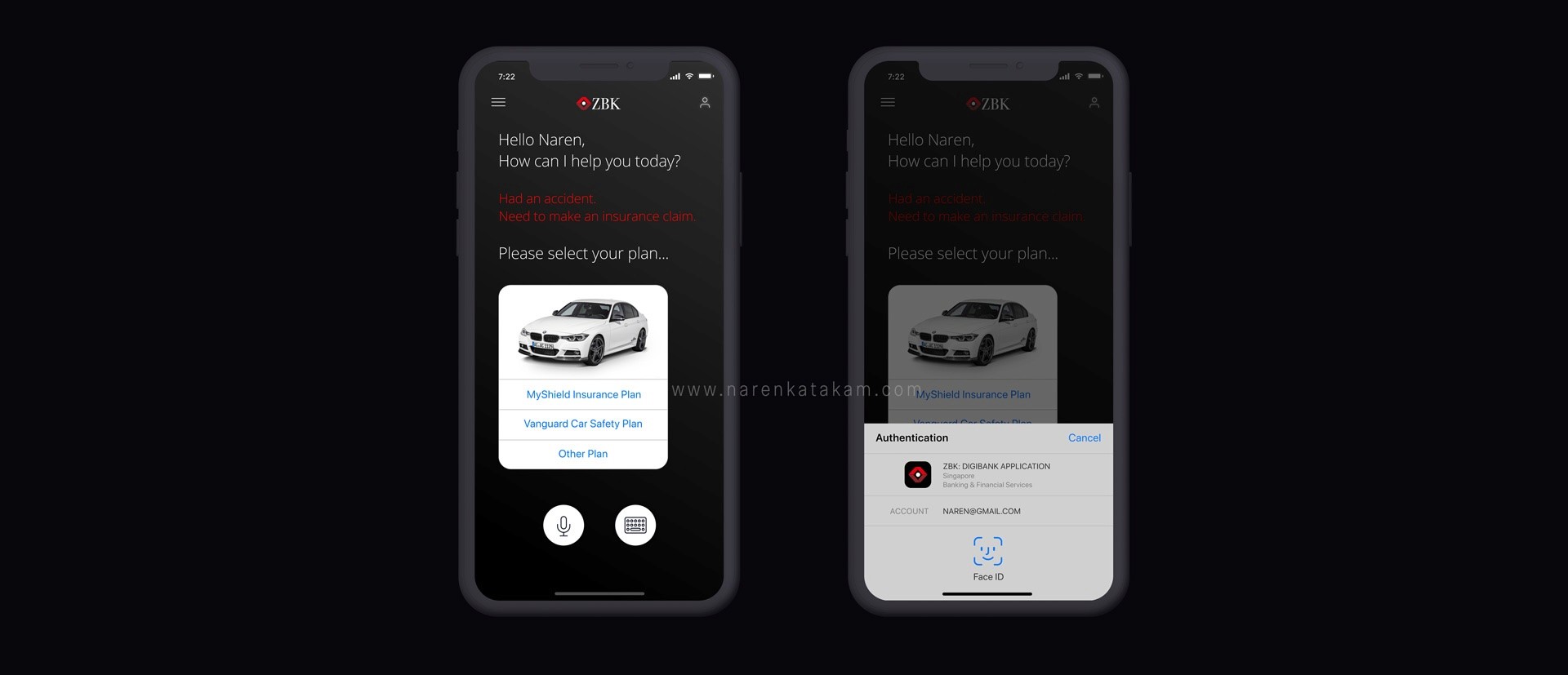

The core concept was banking reimagined as an ambient digital assistant — an AI-powered financial experience that felt less like software and more like a knowledgeable companion. The primary interaction model was conversational — users could query balances, set savings goals, and receive personalised financial advice through natural dialogue, like messaging a knowledgeable friend rather than navigating a banking app.

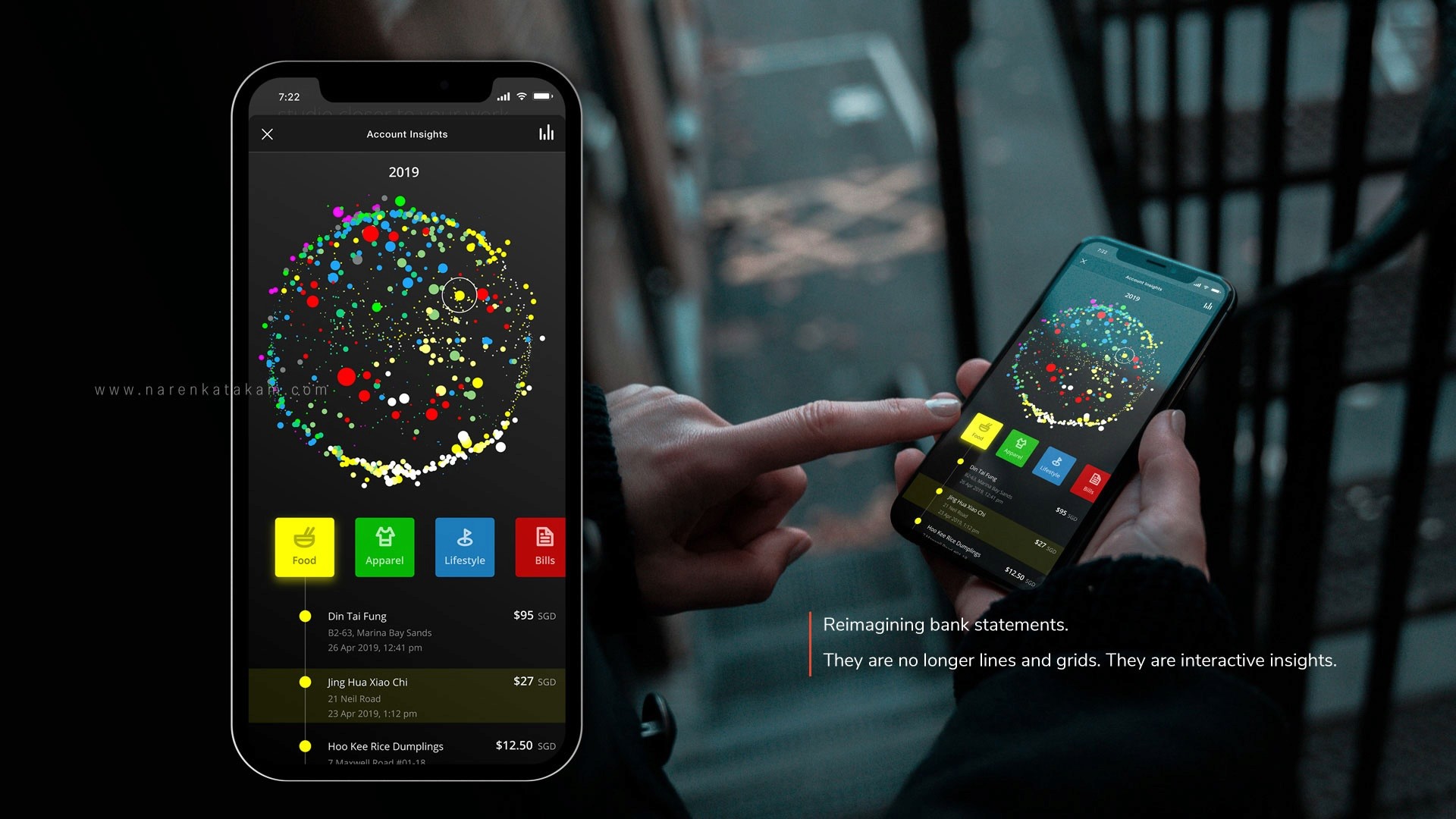

The headline feature was an interactive bubble-based UI that replaced the traditional bank statement. Instead of rows of transactions in a table, users could explore spending across timelines visually, identify patterns intuitively, and surface actionable insights. The interface also featured proactive personalisation: health data-driven insurance suggestions, automated travel expense management, and spending alerts triggered by behavioural patterns rather than arbitrary thresholds. Each of these proactive nudges was a signal capture point — the more the user engaged, the more precise the next suggestion became. The flywheel turned with every interaction.

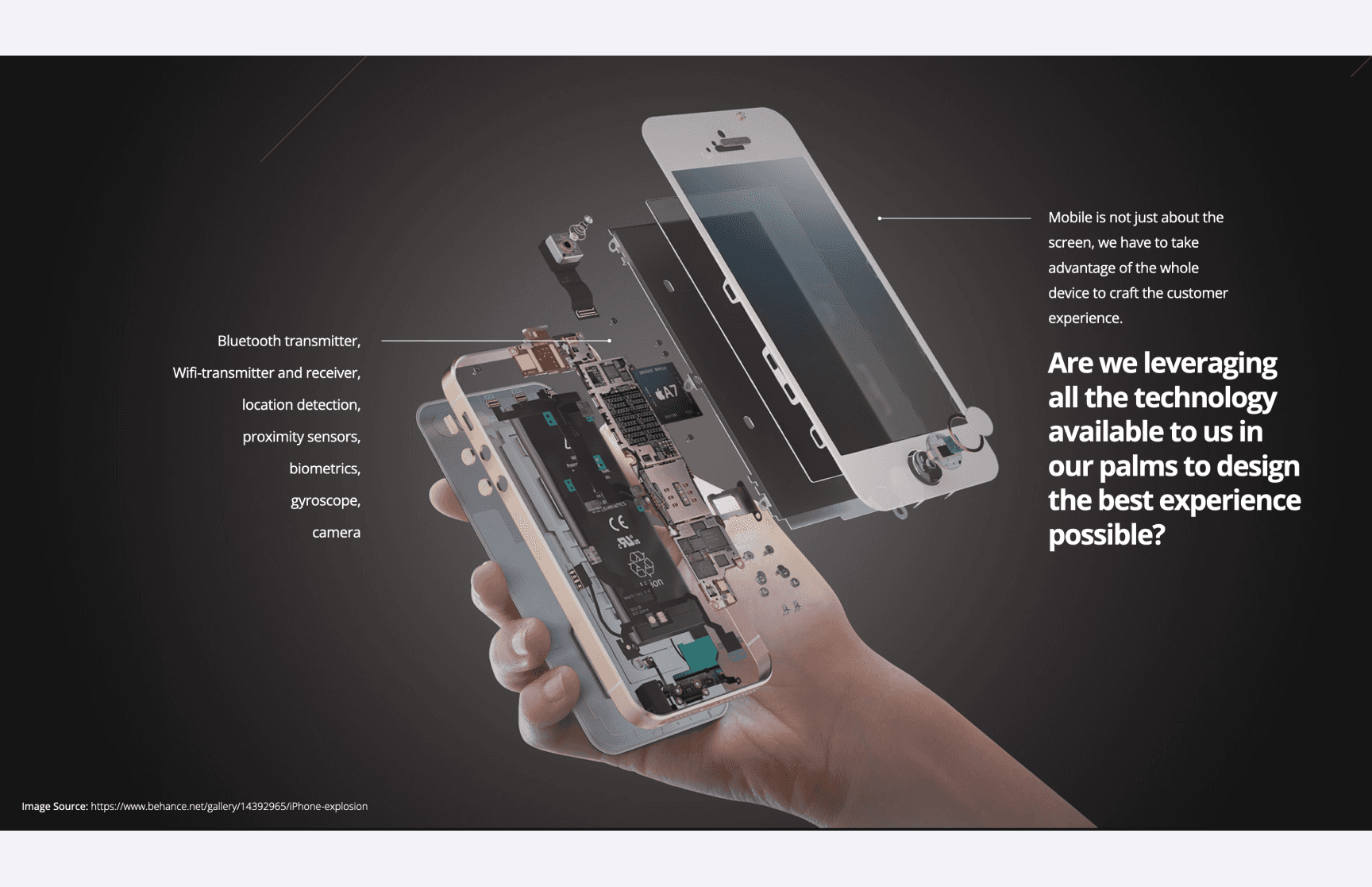

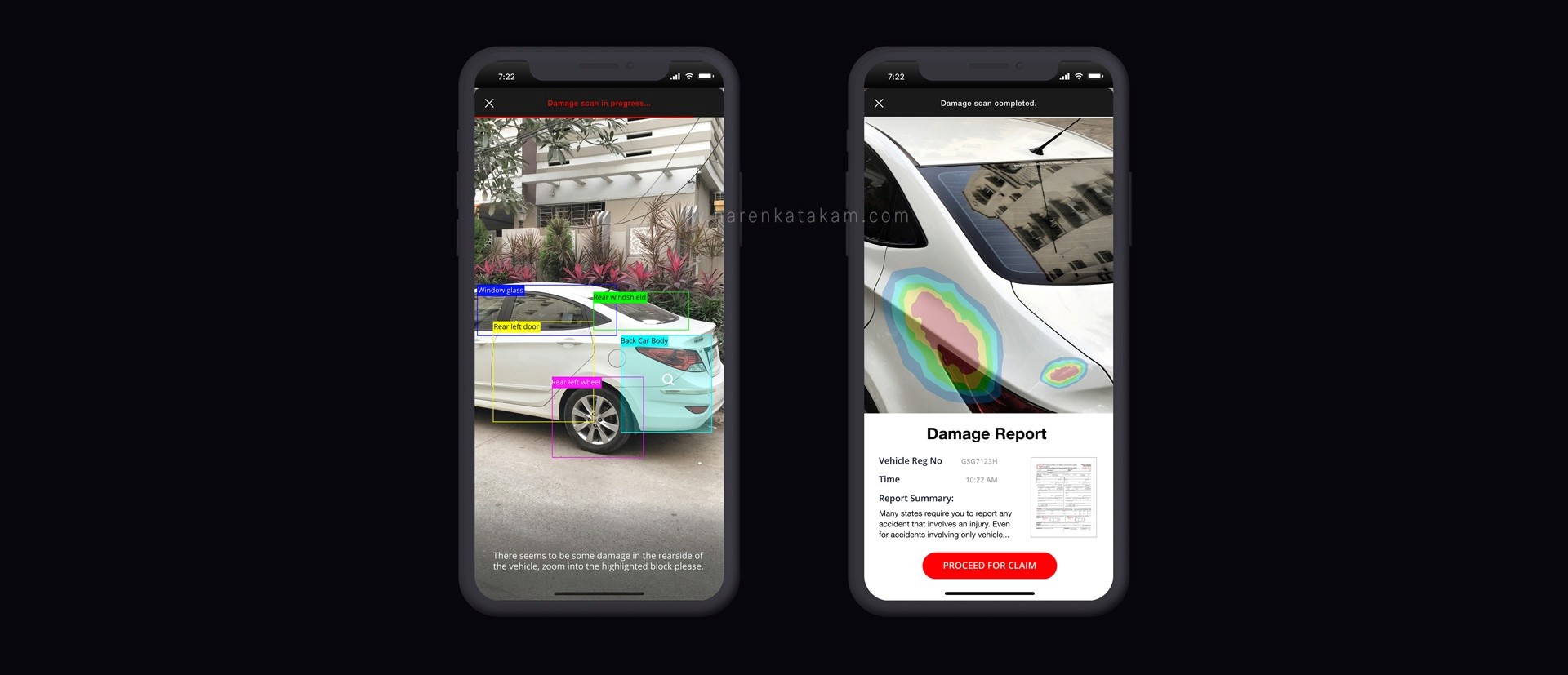

We designed the experience to fully exploit smartphone capabilities — biometric authentication, location detection, proximity sensors, and computer vision — not as gimmicks but as invisible infrastructure. Location awareness meant the app could contextualise your spending in real time. Biometrics eliminated password friction. Computer vision enabled document scanning for expense management. Every sensor capability was mapped to a specific user need, not bolted on for novelty.

The Trust Game

Invisible banking is fundamentally a trust game. Users must surrender behavioural data to receive personalised value. The asymmetry is structural: the bank learns your spending patterns, your routines, your financial anxieties — you don’t see the algorithm.

The entire UX challenge was designing for trustworthy opacity: making the experience feel helpful, not surveilled. Proactive suggestions had to feel like a knowledgeable friend, not a targeted ad. We obsessed over the line between “the bank understands me” and “the bank is watching me.” The difference is almost entirely a design problem — tone of notification copy, timing of suggestions, transparency of reasoning, and always giving the user the sense that they’re in control even when the system is doing the heavy lifting.

This tension — between ambient intelligence and user trust — is the defining constraint of behavioural banking. Get it right, and you build a relationship that deepens with every interaction. Get it wrong, and you’ve built surveillance infrastructure that users will reject at the first scandal.

Results

- Ancillary revenue potential estimated at approximately 33% uplift through algorithmically-driven cross-selling based on actual spending behaviour

- Projected substantial increase in Monthly Active Users and session duration from the conversational interface model

- Improved retention metrics among younger demographics by directly addressing the pain points surfaced in research

- Enhanced Net Promoter Score projections from shifting the banking experience from reactive to anticipatory

- The RASA-powered prototype was demoed by the bank’s CEO at their annual event — it was very well received and helped secure the project as a long-term engagement

What I’d Do Differently Today

The biggest shift is obvious: LLMs have made the conversational banking vision dramatically more achievable. As I explored in The Three Waves of AI, we’ve moved from technology-centric AI to usability-centric AI — and conversational banking sits squarely in that transition. In 2018, conversational UI meant frameworks like RASA — ML-based intent and entity extraction that was capable but required careful training, structured dialogue flows, and significant engineering to handle edge cases. Today, you could build a genuinely intelligent banking assistant that understands context, handles ambiguity, and sustains freeform dialogue — the kind of AI banking experience I was designing toward but couldn’t fully realise with the technology available.

Beyond the AI layer, I’d push harder on two fronts. First, I’d prototype faster with real users rather than validating through expert review. The interactive prototypes were compelling in a boardroom, but I’d want to put them in front of actual millennials doing actual banking tasks within the first two weeks, not after the full concept was polished. Second, I’d design the data strategy as a first-class product decision, not a backend concern. The entire invisible banking thesis depends on algorithmic understanding of user behaviour — and that means the data architecture IS the product architecture. I’d make that explicit from day one rather than treating it as an implementation detail.

Where This Thinking Led

The behavioural data architecture — designing the product around continuous signal capture from daily interactions — became a pattern I applied to personalisation more broadly. When I later designed a recommendation engine for a travel super-app, the same principle held: make every interaction generate signal, and make that signal compound into intelligence. RASA also became my go-to conversational stack in the pre-LLM era — I carried it directly to the aviation data platform, where it powered the natural language query interface for safety data. The invisible bank was where I first understood that data architecture IS product architecture. It was the seed project — the one that taught me how compounding data loops create defensible product advantages. Every case study that follows this one carries DNA from here.

Where This Framework Breaks

Invisible banking breaks on trust. In markets with strong data privacy culture (Europe, increasingly Asia), ambient data collection triggers regulatory friction and user resistance. The design assumes users WANT their bank to anticipate needs — but anticipation without consent is surveillance. The invisible bank only works in a trust environment where the value exchange is transparent and the user retains control.

This isn’t a flaw in the concept — it’s a boundary condition. The same ambient financial services model that feels magical in a high-trust market feels invasive in a low-trust one. Any team applying this framework needs to map the trust landscape before designing the data architecture. The technology is the easy part. The social contract is hard.

Key Takeaway

The banks that win aren’t the ones with the best apps. They’re the ones that figure out how to disappear into the customer’s life — becoming infrastructure rather than a destination. That requires a fundamentally different mobile banking product strategy: designing around behavioural data and ambient intelligence, not screens and features.

FAQ

What does “invisible banking” actually mean as a product strategy?

Invisible banking means designing financial services that integrate seamlessly into daily routines rather than existing as a separate app you consciously open. The bank becomes ambient infrastructure — anticipating needs, automating decisions, and surfacing insights through natural interactions rather than requiring users to navigate traditional banking interfaces. It’s the opposite of “better banking app” — it’s the disappearance of the banking app entirely.

How do you design AI-powered banking without access to customer data early in the process?

You work from behavioural research and published consumer data to map the pain points and desired outcomes first. The AI strategy follows from the user needs, not the other way around. In this project, I mapped specific friction points to specific algorithmic capabilities — you don’t need production data to design the right data strategy, you need a clear understanding of what questions the algorithms need to answer.

What’s the difference between a banking chatbot and a truly conversational banking experience?

A chatbot answers predefined questions. A conversational banking experience is proactive — it initiates interactions based on behavioural patterns, contextualises information using real-time signals like location and spending velocity, and learns from each interaction to become more useful. The 2018 version was constrained by pre-LLM technology, but the design principles hold: the experience should feel like a dialogue with a knowledgeable advisor, not a search through a help menu.

How does invisible banking handle data privacy concerns?

This is the central tension. Ambient financial services require behavioural data to function — the product literally can’t anticipate needs without understanding patterns. The design solution is trustworthy opacity: being transparent about what data is collected and why, giving users granular control, and ensuring every data point captured returns visible value. The moment the value exchange feels one-sided, trust collapses and the model fails.